Licensing Rules Shape Mobile Payment Choices for Sports Bettors

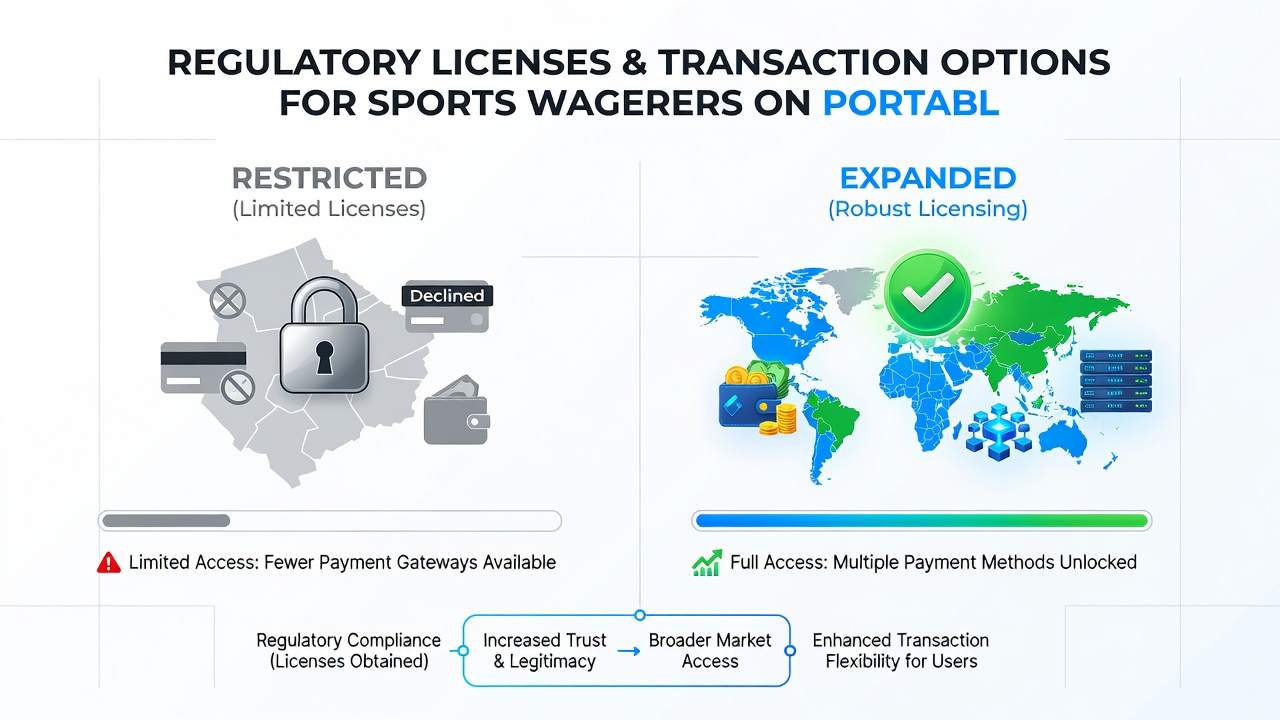

Regulatory licenses establish the boundaries for transaction methods available to sports wagerers who use portable devices, since each jurisdiction imposes distinct requirements on payment processors, banks, and digital wallets that operators must follow to maintain compliance. Operators secure these licenses through applications that detail security protocols, transaction monitoring systems, and partnerships with financial entities, which in turn determine whether users can deposit via credit cards, initiate bank transfers, or access cryptocurrency options on their smartphones and tablets. Data from multiple regulatory bodies shows that licensed platforms in tightly controlled markets often restrict options to traditional banking channels, whereas broader licenses permit integrations with e-wallets and alternative providers that speed up processing times for mobile users.

Variations Across Jurisdictions

State-level licenses in the United States create a patchwork where sports betting apps must align payment gateways with specific rules, for instance those enforced by the Pennsylvania Gaming Control Board require operators to partner only with approved financial institutions that undergo regular audits. This setup limits mobile bettors to debit card deposits and ACH transfers in many cases, while excluding certain cryptocurrency services that lack the required state approvals. Observers note that similar patterns appear in other regions where licenses demand geofencing technology combined with payment verification to prevent unauthorized transactions on portable devices. In Canada the Alcohol and Gaming Commission of Ontario issues licenses that permit a wider array of digital payment solutions, including certain prepaid cards and instant bank transfers, because the framework emphasizes consumer protection through real-time monitoring rather than outright restrictions on payment types.

European markets demonstrate further differences, with licenses from the Malta Gaming Authority allowing operators to integrate multiple international payment processors that support mobile-optimized transactions such as instant e-wallet deposits and withdrawals. These approvals hinge on operators demonstrating compliance with anti-money laundering standards and data encryption requirements tailored to handheld devices. Research indicates that wagerers in these licensed environments encounter fewer barriers when moving funds between their betting accounts and personal banking apps compared to users in regions with narrower licensing scopes.

Impact on Mobile Transaction Speed and Options

Licenses directly influence processing speeds because they dictate which vendors can handle deposits and withdrawals, leading to variations where some mobile apps complete transactions in seconds while others require hours or days for verification. Operators holding licenses that approve direct bank integrations often deliver faster mobile payouts, since those agreements bypass additional third-party checks that slower methods demand. Figures reveal that in jurisdictions with updated licensing standards as of early 2026, apps have incorporated more seamless options like instant verification services that reduce wait times for sports wagerers checking balances on portable devices during live events.

Payment method availability shifts when licenses expire or renew under new conditions, prompting operators to adjust their mobile interfaces accordingly. One study revealed that platforms adapting to revised license terms frequently add or remove cryptocurrency support based on whether the regulatory body has certified specific blockchain providers. Those who've examined transaction logs across different licensed apps find that users in compliant ecosystems gain access to diversified options including digital wallets popular on smartphones, yet they must navigate varying minimum deposit thresholds tied to each license's risk assessment protocols.

Security Protocols Tied to Licenses

Every license incorporates security mandates that affect how transaction data flows through mobile networks, requiring operators to implement encryption standards and fraud detection tools that protect wagerers accessing accounts on portable devices. These protocols often mandate two-factor authentication linked to payment confirmations, which adds steps but reduces unauthorized activity according to reports from industry oversight groups. Licenses granted after thorough reviews tend to support more robust mobile security features, enabling bettors to complete withdrawals without repeated manual verifications that plague less rigorously licensed platforms.

Operators must also comply with license conditions around data storage and cross-border transfers, which restricts certain payment partnerships if the financial entities involved fail to meet jurisdictional standards. This dynamic leads to regional differences where mobile apps in one area offer more transaction flexibility than identical apps operating under stricter licenses elsewhere. Evidence suggests that updates to licensing requirements in mid-2026 have prompted several platforms to expand approved payment lists for portable device users, incorporating additional e-wallet providers that align with enhanced verification rules.

Conclusion

Regulatory licenses continue to define the transaction landscape for sports wagerers on portable devices by setting approval criteria for payment methods, security measures, and processing timelines across global markets. Those who track these developments see ongoing adjustments as operators respond to license renewals and new regulatory expectations, resulting in evolving options that reflect each jurisdiction's priorities around compliance and user access. Data from diverse sources including government agencies and research institutions underscores how these frameworks shape daily interactions between bettors and their mobile betting applications.